Does Debt Consolidation Hurt Your Credit Score?

Why Go Through the Stress of Debt?

Owing in this generation has been one of the problems of people. A lot of people are living a low-key life as a result of the amount of money they owe, some do not have freedom to go to some certain place in order for their faces not to be recognized. Some are even summoned at the police station every now and then.

In order to be free from this debt, some have taken a bold step to go for debt consolidation. That is, paying up your debt at once, at a goal. Paying your debt at once might not be an easy task but read through as I help you.

Definition of Debt Consolidation

It means making an adequate plan on how you pay up the money you are owing at once. It involves you combine various outstanding debt and paying it up at once, it can be through loan, your credit score or any other means.

In this article, we will get to know if debt consolidation can hurt your credit score.

What to Know About Credit Score

Your credit score is the total amount of your credit history. Credit score is usually in three figures.

This credit score is very important because it is this credit score that will let you know if you can get a loan and what the interest will be. Your credit score depends on your credit history.

Your credit scores determine your creditworthiness. It is through your credit score that those who want to loan you will know if they can loan you.

A good credit score is important for getting favourable interest and loans. Read through as we get clearer on this.

Purpose Of Credit Score

- It is used to decide whether someone should be approved for a loan or not.

- Credit score is used to determine the interest rate you will be charged and your credit limit.

- Insurance companies and land/ house owners can also consider your credit score when they make decisions.

General Ranges Of Credit Scores

- 740 and above: Excellent credit

- 670 – 739: Very good credit

- 630 – 669: Good credit

- 580 – 629: Fair credit

- Below 580: Poor credit

How To Maintain a Good Credit Score

- Ensure you make all your payment on time.

- Make your credit utilization low.

- Do not apply for too much credit at once.

- Review your credit reports to avoid mistakes and errors.

With all that is written above, I’m sure you understand what the credit score is, so, let us move to what we have been waiting for.

Does Debt Consolidation Hurt Your Credit Score?

In my opinion, I’ll say yes and no. Debt consolidation can hurt your credit score and at the same time, it cannot hurt your credit score. It has both positive and negative effects on your credit score depending on a variety of factors.

It is important you study the positive and negative effects for you to determine if it is right for you.

Positive Effect Of Debt Consolidation

- The mechanics of paying your debt at once:

Debt consolidation has to do with taking a new loan or using a balance credit card to pay your existing debt. It makes your debt single and it gives you a favorable term, that is the interest payment is reduced, and you are given a longer repayment plan that works with you. The aim of this is to make your debt manageable.

- Lower interest rates:

Consolidation of loans always offer lower interest rates compared to credit cards. They help in reducing your overall interest payments and freeing up enough money to make payment for the debt faster. Faster debt payment determines your credit score overtime.

- Debt to income ratio:

When your consolidation finally reduces your overall debt compared to your income, then your debt to income ratio improves, which is a reliable positive factor for your credit score.

- Monitoring your credit progress:

There is a need for you to monitor your credit progress all the time. Ensure that you confirm all the accounts are reported regularly and are accurately written so there won’t be any form of error or mistake.

Negative Effect Of Debt Consolidation

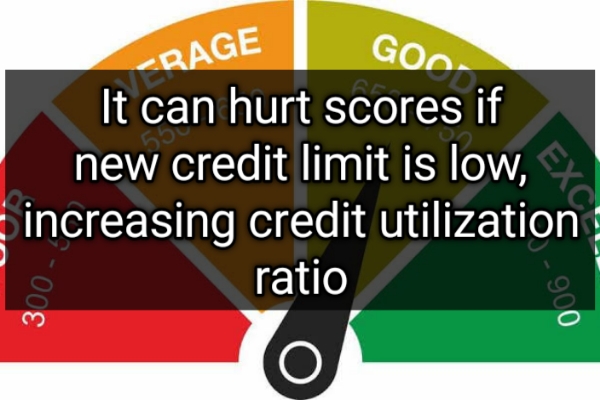

The effect of credit utilization:

An important factor that determines your credit utilization is your credit score. That is the way you use your credits and income, gain is your credit score meaning, it is what you worth ,what you have, and what you can afford. But if your new card credit limit is low, your credit utilization ratio might increase.

Consolidating your debt may result in an increase in your credit utilization as the new credit loan may have its limits. However, as you continue to make payments , there will be improvement as time goes on.

- Make credit inquiries and impact:

A process you must pass through in paying your debt at once is starting a credit inquiry when you apply for a new loan or credit card. The action might be a hard inquiry in your credit report.

If it is a hard inquiry, your credit report might be affected as it might tend to reduce your credit score points. It is usually short term on your credit score.

Credit scores are created so that consumers know that they can shop around for favorable items.

- Closing your old accounts:

Closing down your old credit card accounts in consolidation can bring about a decrease in your score, bringing about a shorter credit history and credit mix factors.

Conclusion

Remember, whatsoever you plan to do, think indepthly regarding your debt consolidation, ensure you go through the factors to see what works for you and what doesn’t work.

If you are confused, you can meet and consult a financial advisor or a credit counselor to discuss with and guide you on what to do.