After I decided getting a loan was the next option, the only thing on my mind was how to deal with the interest rates because I could still remember vividly how my friend had taken a loan about a year ago and the interest almost brought his financial strength to nothing

His experience made me scared of loans until someone informed me that I could find credit facilities with lower rates so I began a journey to find the one that my financial capacity could effortlessly shoulder.

You’ll agree with me that when it comes to taking out a loan, interest rates are a major factor in determining the total cost.

So Choosing a loan with the lowest interest rate can save us hundreds or even thousands of dollars over the life of the loan.

Welcome to this comprehensive guide, we’ll compare interest rates across different loan types to identify which option usually comes with the lowest rates.

We’ll also look at factors that impact loan pricing, provide tips for getting the best rate, and give recommendations for low interest loans.

Table of Contents

Understanding Interest Rate

Before diving into the main reason why we are here, it is important to know what an interest rate is;

The interest rate is the cost you pay to borrow money through a loan. Rates can vary greatly depending on the type of loan, your finances, the lender, and market conditions.

Comparing several options is the only way to ensure you’re getting the lowest rate possible.

Now, For US residents, certain types of loans tend to offer lower interest rates than others.

Federal student loans and VA mortgages consistently come with lower rates compared to alternatives.

We’ll explore why that is and look at other financing options that can provide low cost borrowing.

When you understand the current interest rate trends and which loans offer you the best terms, you can make smart financing decisions and keep borrowing costs in check.

Average Interest Rates by Loan Type

Below we have provided an overview of current average interest rates for common loan products in the US:

Mortgages

Conventional: 6.33%

FHA: 6.5%

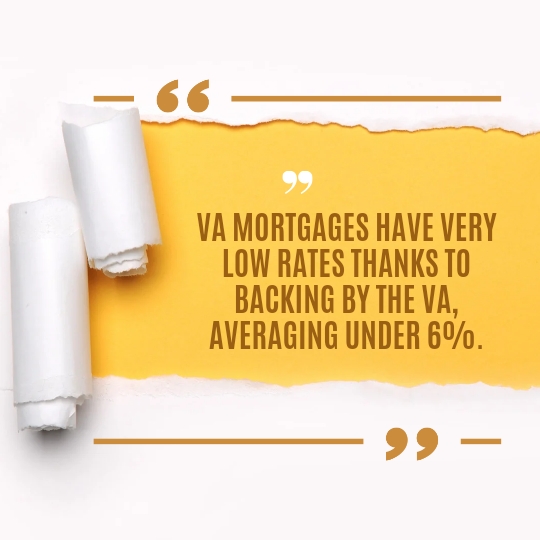

VA: 5.85%

Jumbo: 5.66%

Auto Loans

New vehicle: 6.28%

Used vehicle: 9.47%

Personal Loans

36-month term: 11.39%

60-month term: 12.88%

Student Loans

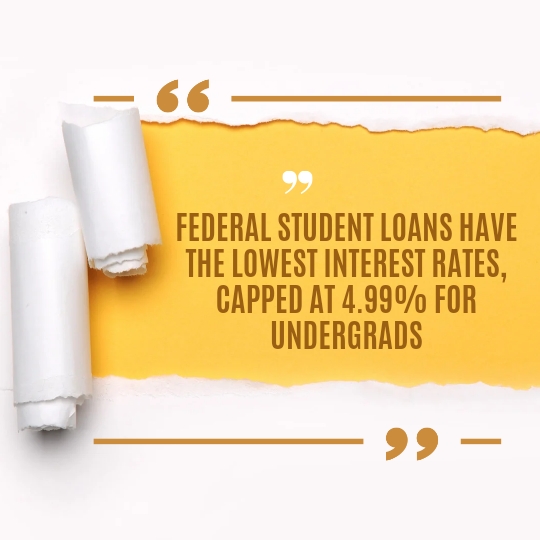

Undergraduate federal: 4.99%

Graduate federal: 6.54%

Private student loans: 8.63%

Credit cards

15.01%

As you can see, interest rates can vary significantly depending on the type of financing you need.

Federal student loans and VA home loans consistently offer you the lowest rates.

Now, Let’s take a closer look at why that is.

Federal Student Loans Have the Lowest Rates

For US students looking to borrow money for college, the federal student loans almost always provide the cheapest options for them .

The Rates for undergraduate federal loans are capped at 4.99% APR for the 2022-23 academic year.

The Graduate federal loans are only slightly higher at 6.54% APR.

These rates are exceptionally low because of the federal government backing these loans. By removing the risk for private lenders, the government can offer students very favorable terms for loans.

It’ll interest you to know that even the highest rate for federal loans is lower than the average for private student loans, which currently sit around 8-9% APR.

This is Because private lenders don’t receive government guarantees, so they must charge higher rates to offset the risk of default.

The Federal student loan rates are also fixed for the life of the loan, unlike private loans which often have variable rates. So Borrowing from the federal program provides exceptional rates and protections you can’t find elsewhere.

VA Mortgages Have the Lowest Rates

After student loans, there’s the VA home loans and it offers the next lowest rates, currently averaging around 5.85% APR.

These mortgages are guaranteed by the Department of Veterans Affairs, making them very low risk for lenders.

With a VA loan, you can enjoy the following:

- You can qualify with zero down payment

- There are No monthly mortgage insurance required

- Your funding fee can be rolled into the loan

Because lenders face less risk providing VA mortgages, they can offer lower rates compared to conventional loans. VA rates are now below both conventional and FHA mortgage rates.

Only jumbo mortgages currently have lower average rates than VA loans. But jumbos require you to make a down payment of at least 20% and have strict credit score and income requirements.

VA mortgages are accessible to more buyers.

Factors That Impact Loan Interest Rates

When reviewing your loan options, it is important to keep in mind that advertised rates are just averages.

Your specific rate will depend on the following :

- Your credit – Borrowers with higher scores tend to get lower rates across all loans. So Maintaining excellent credit should be priority #1.

- Loan term – Be aware Shorter terms usually have lower rates. 15-year mortgages and 3-year auto loans offer you lower rates than longer terms.

- Your finances –Your Income, assets, debt-to-income ratio and down payment amount all impact qualification and pricing.

- Loan type and size – As enunciated above, Government and secured loans are lower risk, as are smaller loan amounts. These factors lead to lower rates.

- Economic factors – Note Rates trend up when the Federal Reserve raises its federal funds rate, as it has been doing in 2022.

- Lender – Different lenders offer different rates, that is why you Compare different options as they vary from one another.

Having addressed that, Let’s have a look at tips for locking in the lowest rate on a personal, auto, mortgage or student loan.

How to Get the Lowest Interest Rate

While it is normal for some borrowers to always receive lower rates thanks to stellar credit and finances, anyone can improve their odds of getting better pricing by following these tips listed below:

- Check your credit reports – You need to Ensure there are no errors dragging down your scores before applying.

- Lower credit utilization – When you Have balances above 30% of limits, it will reduce your scores so try to Pay down cards.

- Avoid new credit – New accounts tend to lower your average account age, so wait to apply for financing until you need it.

- Shop lenders – It is imperative to Compare loan interest rates and fees from multiple lenders. Get pre-qualified to find the best deals for you.

- Improve your debt-to-income ratio – Your DTI also impacts qualification and pricing . So Pay down debts to improve this ratio.

- Make a larger down payment – When you Put more money down on a home or car, it makes the loan lower risk for a lender.

- Enroll in auto-pay discounts – Most lenders offer you an interest rate reduction when you enroll in auto-pay.

- Ask about rate-match programs – Another way is to find out if the lender will match a competitor’s lower rate.

Effectively applying these strategies can help you land the lowest interest rate possible on a personal loan, auto financing, mortgage or student loan.

Loans with the Lowest Interest Rates

Based on current rate trends and averages, we have provided below the loans that tend to offer the lowest interest rates:

Federal student loans – Both undergraduate and graduate federal student loans offer rates below 7%, with undergraduate loans capped at 4.99%. Be aware that Private student loans can’t match these rates.

VA mortgages – VA home loans let buyers skip down payments and mortgage insurance, thanks to the VA backing. Rates average below 6% and beat out conventional mortgages.

15-year mortgages – The shorter term leads to lower rates compared to 30-year mortgages. The lower overall interest savings help you offset the higher monthly payments.

New auto loans – New car loans offer the lowest rates for auto financing, averaging around 6% APR currently. Usually Used car loans are much higher.

Short-term personal loans – Loans with terms under 3 years will offer the lowest rates from online lenders. But you’ll need to weigh the higher monthly payments against the interest savings.

Should You Choose a Loan Based on Rate Alone?

I know all we’ve been talking about since has been on rates and how important it is to consider before taking loans but it’s important to ask if it should necessarily be the only criteria one has to consider when taking a loan.

The answer to that is “no”, so You’ll also want to consider:

Fees – Note that Lower rates don’t always mean lower total costs when factoring in fees like origination charges.

Qualification – Federal student loans are accessible even with little/no credit. However, Jumbo mortgages have high standards you’ll have to meet to obtain the loan .

Cash flow – It is true that Lower rates over longer terms spread costs out but the result is that more interest is paid overall.

Perks – Some lenders offer you valuable benefits like delayed payments or unemployment protection, so you need to consider these things.

Risks – Federal loans pose much less risk to borrowers than private options that lack protections, so know this before applying for one .

To make the best decision for your situation, it is important for you to look at the whole package – not just the interest rate.

Make sure you can actually qualify and comfortably handle the monthly payments so you don’t get into debts that would become choking.

While rate is important, please don’t sacrifice other important factors just to get the lowest APR possible.

Which Loan is Right for You?

Every borrower’s needs and financial situation is different that’s why we all need to Consider the following when deciding which type of loan works best aligns with our individual needs :

Home purchase – A conventional, VA, or FHA mortgage allows you to finance a home purchase. But you need to Compare the government-backed options to have access to lowest rates.

Auto purchase – New car loans offer lower rates but used car loans cost less overall. So it is advisable to Get pre-approved to find the best financing.

Debt consolidation – Personal loans options allow borrowers to consolidate high-interest credit card balances at lower rates, if you qualify.

College costs – Federal student loans provide the cheapest way to pay for an undergraduate or graduate degree. Make sure you Max out this borrowing first before considering private loans.

Home improvements – Personal loans or HELOCs allow you to tap home equity to fund renovations at competitive rates. So when you want to make improvements to your house, you know where to go

Medical expenses – Personal loans can help cover large out-of-pocket medical costs at reasonable rates compared to credit cards. So that is settled now.

Starting a business – When you wish to start a business, you should try out SBA loans. They encourage small business lending by reducing risks for banks.

Their rates are however competitive but you’ll need good credit and collateral.

Credit card refinancing – Balance transfer cards allow you to consolidate card debt at a lower promotional APR for a limited period of time.

It is worthy to note that No single loan provides the best rates or terms across the board.

You’ll have to consider the purpose of the financing and your financial situation to choose the loan that works best for you.

Focus on options you’re likely to actually qualify for. Then compare the total costs of it, including fees and not just interest rates.

No worries, With some research, you can find an affordable loan that meets your needs.

Final Thoughts

For you to Find the loan option with the lowest interest rate, it involves understanding the typical rates for different loan types and the factors that impact pricing.

Generally federal student loans and VA mortgages offer the lowest rates thanks to government backing.

Beyond the interest rates they provide, you need to also weigh eligibility requirements, total costs, loan terms, and risks when deciding on financing.

Your personal financial situation should guide which type of loan makes sense for your needs and budget.

If you effectively Utilize these tips and average rate data, you can compare loan products and lenders to secure the most affordable financing possible for you.

Have it in mind that a low rate isn’t worthwhile if the loan isn’t a good fit for your situation. So try to Keep both big picture factors and rate details in mind to find the best loan match.